Chapter 3: Feature Engineering

Activity 10: Calculating Time series Feature – Binning

Solution:

- Load the caret library:

#Time series features

library(caret)

#Install caret if not installed

#install.packages('caret')

- Load the GermanCredit dataset:

GermanCredit = read.csv("GermanCredit.csv")

duration<- GermanCredit$Duration #take the duration column

- Check the data summary as follows:

summary(duration)

The output is as follows:

Figure 3.27: The summary of the Duration values of German Credit dataset

- Load the ggplot2 library:

library(ggplot2)

- Plot using the command:

ggplot(data=GermanCredit, aes(x=GermanCredit$Duration)) +

geom_density(fill='lightblue') +

geom_rug() +

labs(x='mean Duration')

The output is as follows:

Figure 3.28: Plot of the duration vs density

- Create bins:

#Creating Bins

# set up boundaries for intervals/bins

breaks <- c(0,10,20,30,40,50,60,70,80)

- Create labels:

# specify interval/bin labels

labels <- c("<10", "10-20", "20-30", "30-40", "40-50", "50-60", "60-70", "70-80")

- Bucket the datapoints into the bins.

# bucketing data points into bins

bins <- cut(duration, breaks, include.lowest = T, right=FALSE, labels=labels)

- Find the number of elements in each bin:

# inspect bins

summary(bins)

The output is as follows:

summary(bins)

<10 10-20 20-30 30-40 40-50 50-60 60-70 70-80

143 403 241 131 66 2 13 1

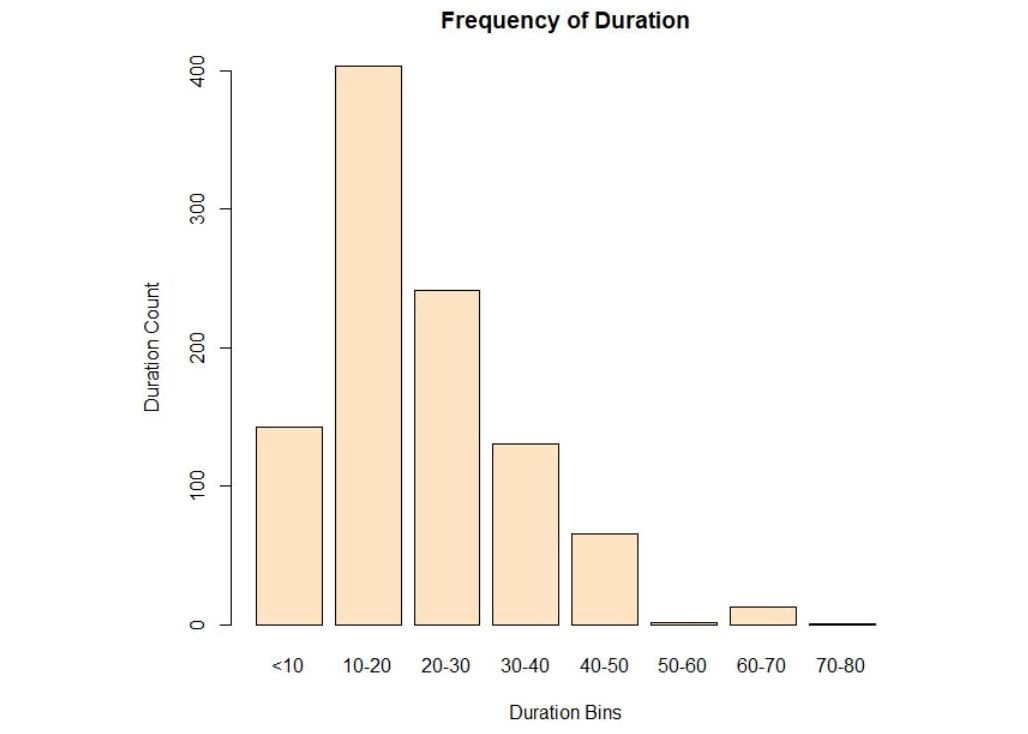

- Plot the bins:

#Ploting the bins

plot(bins, main="Frequency of Duration", ylab="Duration Count", xlab="Duration Bins",col="bisque")

The output is as follows:

Figure 3.29: Plot of duration in bins

We can conclude that the maximum number of customers are within the range of 10 to 20.

Activity 11: Identifying Skewness

Solution:

- Load the library mlbench.

#Skewness

library(mlbench)

library(e1071)

- Load the PrimaIndainsDiabetes data.

PimaIndiansDiabetes = read.csv("PimaIndiansDiabetes.csv")

- Print the skewness of the glucose column, using the skewness() function.

#Printing the skewness of the columns

#Not skewed

skewness(PimaIndiansDiabetes$glucose)

The output is as follows:

[1] 0.1730754

- Plot the histogram using the histogram() function.

histogram(PimaIndiansDiabetes$glucose)

The output is as follows:

Figure 3.30: Histogram of the glucose values of the PrimaIndainsGlucose dataset

A negative skewness value means that the data is skewed to the left and a positive skewness value means that the data is skewed to the right. Since the value here is 0.17, the data is neither completely left or right skewed. Therefore, it is not skewed.

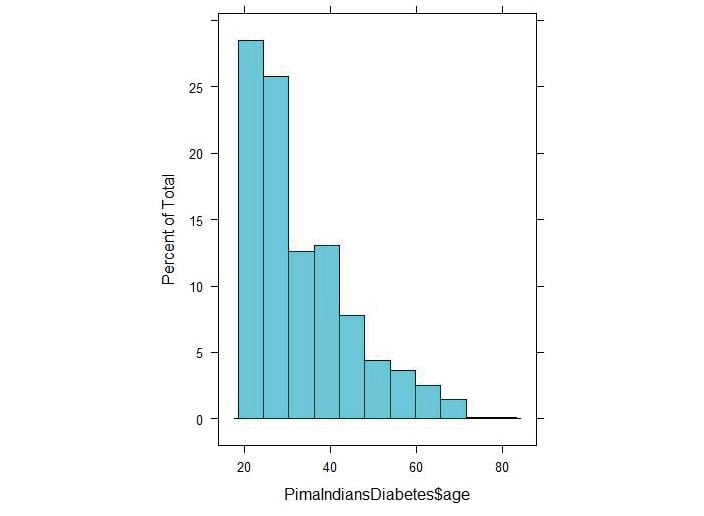

- Find the skewness of the age column using the skewness() function.

#Highly skewed

skewness(PimaIndiansDiabetes$age)

The output is as follows:

[1] 1.125188

- Plot the histogram using the histogram() function.

histogram(PimaIndiansDiabetes$age)

The output is as follows:

Figure 3.31: Histogram of the age values of the PrimaIndiansDiabetes dataset

The positive skewness value means that it is skewed to the right as we can see above.

Activity 12: Generating PCA

Solution:

- Load the GermanCredit data.

#PCA Analysis

data(GermanCredit)

- Create a subset of first 9 columns into another variable names GermanCredit_subset

#Use the German Credit Data

GermanCredit_subset <- GermanCredit[,1:9]

- Find the principal components:

#Find out the Principal components

principal_components <- prcomp(x = GermanCredit_subset, scale. = T)

- Print the principal components:

#Print the principal components

print(principal_components)

The output is as follows:

Standard deviations (1, .., p=9):

[1] 1.3505916 1.2008442 1.1084157 0.9721503 0.9459586

0.9317018 0.9106746 0.8345178 0.5211137

Rotation (n x k) = (9 x 9):

Figure 3.32: Histogram of the age values of the PrimaIndiansDiabetes dataset

Therefore, by using principal component analysis we can identify the top nine principal components in the dataset. These components are calculated from multiple fields and they can be used as features on their own.

Activity 13: Implementing the Random Forest Approach

Solution:

- Load the GermanCredit data:

data(GermanCredit)

- Create a subset to load the first ten columns into GermanCredit_subset.

GermanCredit_subset <- GermanCredit[,1:10]

- Attach the randomForest package:

library(randomForest)

- Train a random forest model using random_forest =randomForest(Class~., data=GermanCredit_subset):

random_forest = randomForest(Class~., data=GermanCredit_subset)

- Invoke importance() for the trained random_forest:

# Create an importance based on mean decreasing gini

importance(random_forest)

The output is as follows:

importance(random_forest)

MeanDecreaseGini

Duration 70.380265

Amount 121.458790

InstallmentRatePercentage 27.048517

ResidenceDuration 30.409254

Age 86.476017

NumberExistingCredits 18.746057

NumberPeopleMaintenance 12.026969

Telephone 15.581802

ForeignWorker 2.888387

- Use the varImp() function to view the list of important variables.

varImp(random_forest)

The output is as follows:

Overall

Duration 70.380265

Amount 121.458790

InstallmentRatePercentage 27.048517

ResidenceDuration 30.409254

Age 86.476017

NumberExistingCredits 18.746057

NumberPeopleMaintenance 12.026969

Telephone 15.581802

ForeignWorker 2.888387

In this activity, we built a random forest model and used it to see the importance of each variable in a dataset. The variables with higher scores are considered more important. Having done this, we can sort by importance and choose the top 5 or top 10 for the model or set a threshold for importance and choose all the variables that meet the threshold.

Activity 14: Selecting Features Using Variable Importance

Solution:

- Install the following packages:

install.packages("rpart")

library(rpart)

library(caret)

set.seed(10)

- Load the GermanCredit dataset:

data(GermanCredit)

- Create a subset to load the first ten columns into GermanCredit_subset:

GermanCredit_subset <- GermanCredit[,1:10]

- Train an rpart model using rPartMod <- train(Class ~ ., data=GermanCredit_subset, method="rpart"):

#Train a rpart model

rPartMod <- train(Class ~ ., data=GermanCredit_subset, method="rpart")

- Invoke the varImp() function, as in rpartImp <- varImp(rPartMod).

#Find variable importance

rpartImp <- varImp(rPartMod)

- Print rpartImp.

#Print variable importance

print(rpartImp)

The output is as follows:

rpart variable importance

Overall

Amount 100.000

Duration 89.670

Age 75.229

ForeignWorker 22.055

InstallmentRatePercentage 17.288

Telephone 7.813

ResidenceDuration 4.471

NumberExistingCredits 0.000

NumberPeopleMaintenance 0.000

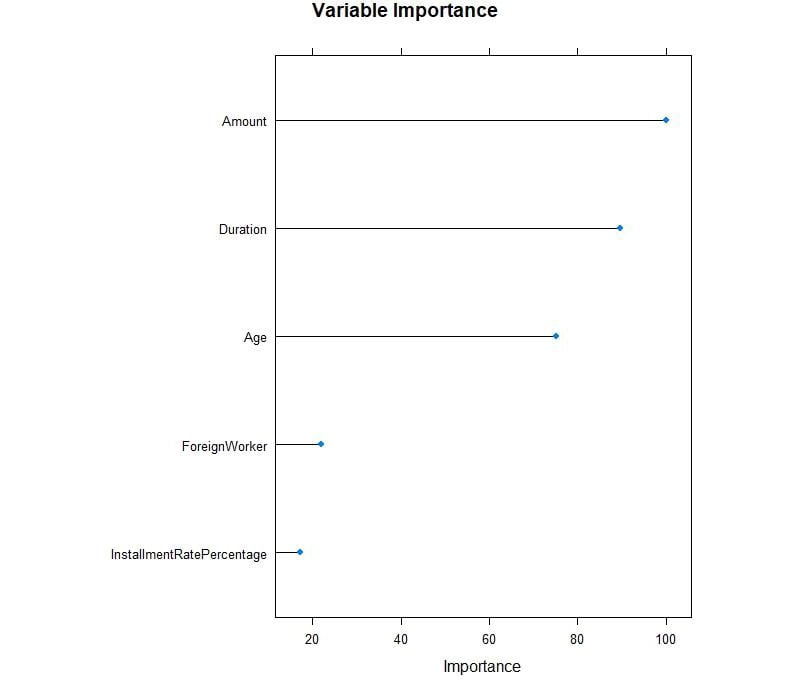

- Plot rpartImp using plot().

#Plot top 5 variable importance

plot(rpartImp, top = 5, main='Variable Importance')

The output is as follows:

Figure 3.33: Variable importance for the fields

From the preceding plot, we can observe that Amount, Duration, and Age have high importance values.